Time and again, our insurance member companies come across well-meaning policyholders who inadvertently make dishonest insurance claims. It can be easy to do. We don’t often have a need to make a claim. When we do need to make a claim, the process of doing so can sometimes get technical, include requests for supporting documentation and in some instances, feel like an overwhelming process.

In times like these, it can be simpler for policyholders who are struggling to complete their claim paperwork to ask the advice of friends, family, flatmates, colleagues or neighbours. However, well-meaning advice about what you should and shouldn’t include in an insurance claim isn’t always correct, and can result in inaccurate claims.

When you have any questions about an insurance claim, your first point of contact should be your insurer. Their customer service team will happily run you through the claim process, and ensure you make an accurate claim.

This article will be helpful for when you next make an insurance claim. We’ll assess what is and what isn’t an honest claim and tackle soft and hard fraud too.

What is an honest claim?

Not surprisingly, an honest claim is when you complete your claim application honestly, and accurately. Rather than leaving gaps or guessing details, phone your insurer to ask them for advice on how to answer that particular question.

Supplying proof of purchase or other relevant receipts are also good ways to ensure your claim is complete.

What isn’t an honest claim?

Dishonest claims can inadvertently and purposefully occur in a number of ways.

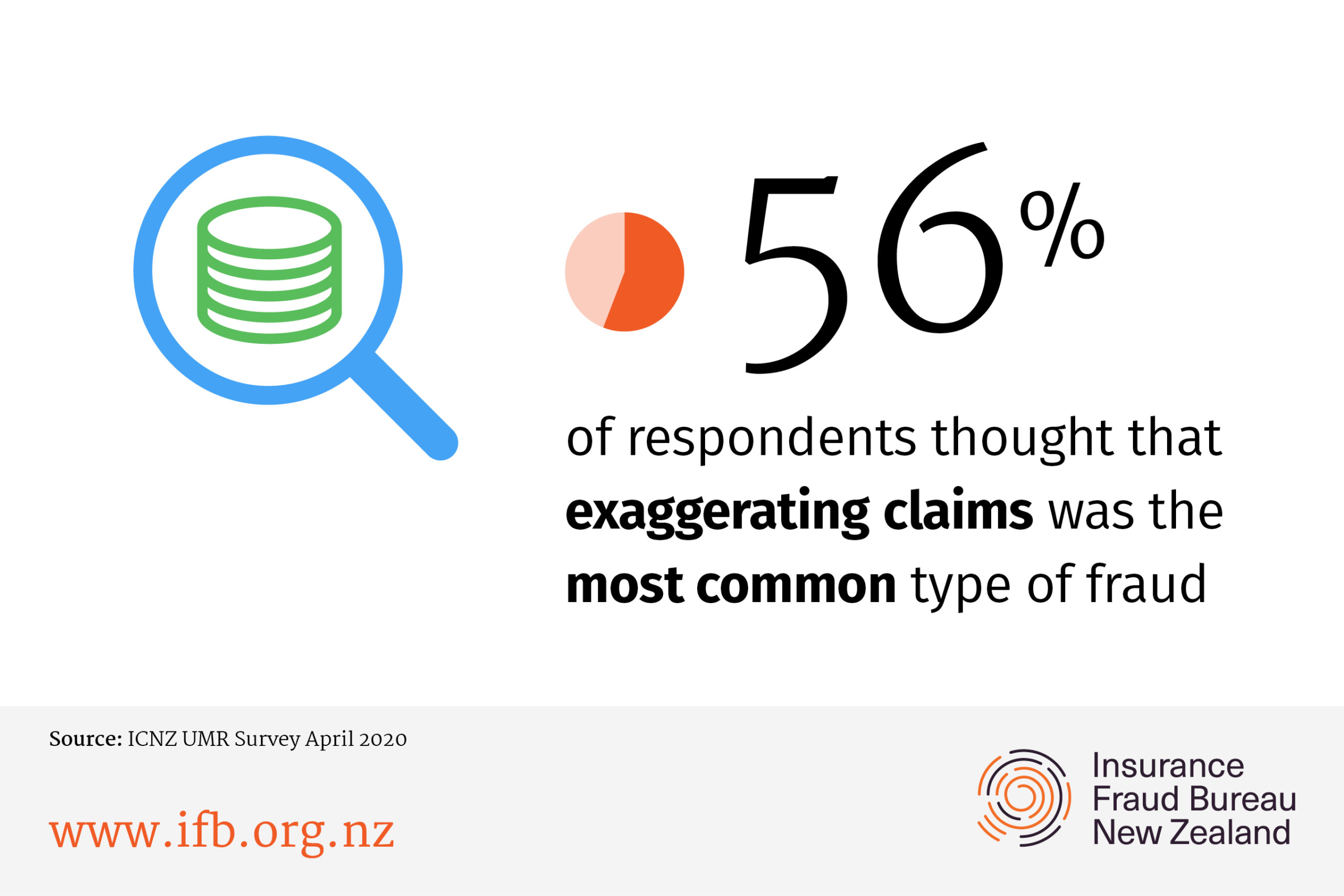

1. Exaggerating claims

Let’s take the example of a house burglary. If you’re not 100% sure of what was stolen and “guess” what was taken, or exaggerate the number of items that were stolen, the insurance industry considers that an exaggeration of an insurance claim. Or you might think a stolen item is worth a set amount, when its value has actually depreciated since you bought it. All of these are examples are insurance fraud.

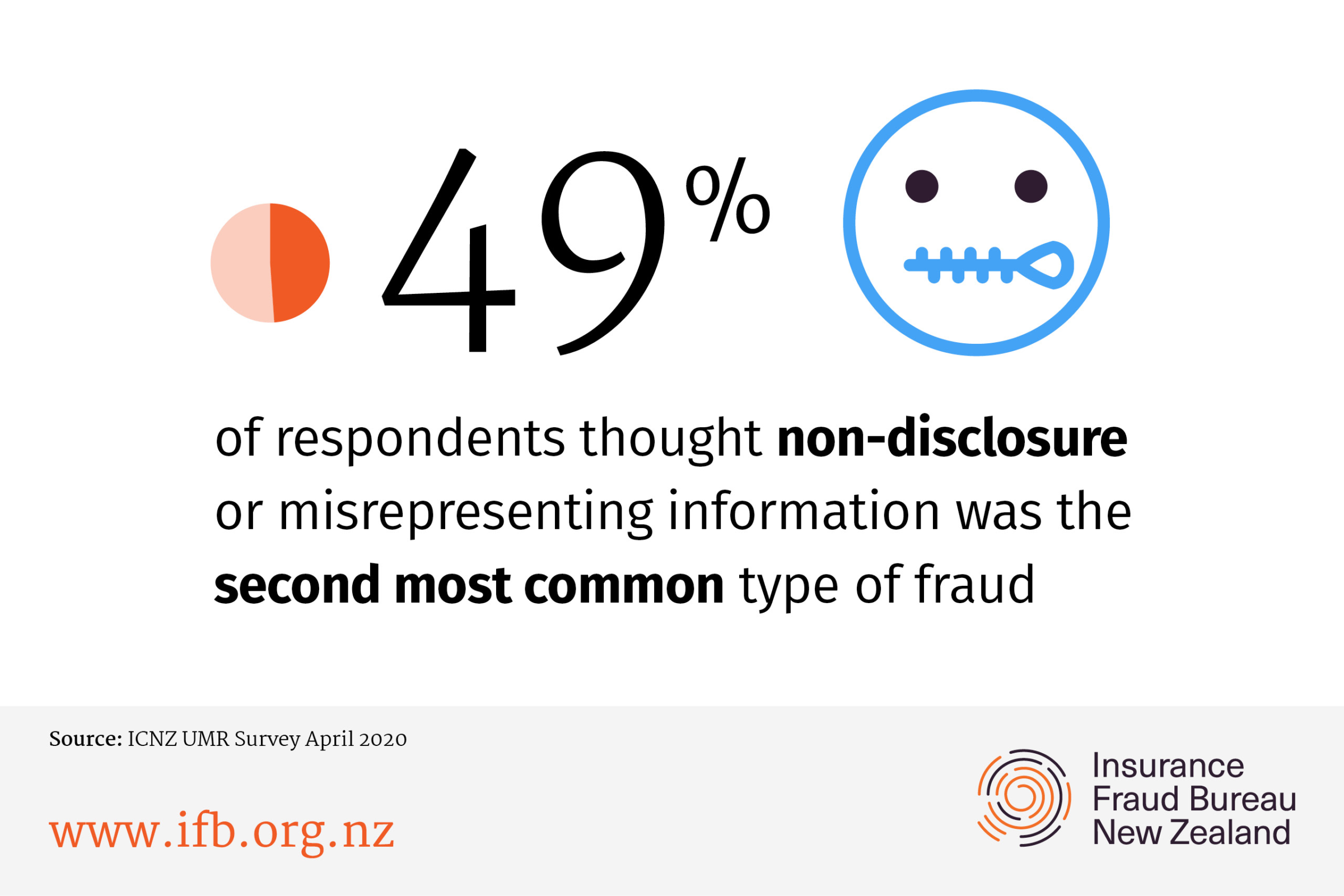

2. Non-disclosure

By choosing to not provide information, because you think it may be detrimental to your claim, is considered non-disclosure. An example might be not telling your current insurer about previously declined claims with other insurers, in the thought that you will secure new insurance cover – this is also insurance fraud.

Some insurers share claim information through an anti-fraud detection tool called the Insurance Claims Register (ICR). The ICR is a database that houses claims histories so that insurers can see claiming behaviours.

3. Mis-representing information

Some people may purposefully damage a valuable item, such as their iPhone, in order to make a claim and access some money when they are in financial difficulty. Stating the damage was accidental is insurance fraud.

There are a number of ways a policyholder may choose to be dishonest in their insurance claim. The key pillars in the psychology of fraud include:

- Motivation – financial stress or a sense of entitlement may encourage someone to make a dishonest claim.

- Opportunity – the opportunity to make a claim provides people a unique way to take advantage of a situation that has a perceived low risk, but a high financial gain

- Rationalisation – justifying the decision to be dishonest is an important part of going through with a dishonest claim. Some people feel that “insurers make a lot of money; they can afford it” and “I won’t get enough money to replace my damaged item with the one I want”. For some, they can be encouraged by someone they trust to take advantage of the opportunity to make a claim.

You can find out more information about what causes fraud on our website.

The difference between soft and hard fraud

Hard fraud is a planned and deliberate attempt to make a false insurance claim, or apply for a new policy under false pretences. Examples of hard fraud are staging a burglary or deliberately crashing a vehicle with the specific purpose of making an insurance claim. This type of fraud is often repeated, and other people can be asked to get involved too.

On the other hand, soft fraud is often committed when a policyholder has an opportunity to do so. For example, they are in a position to make a claim and stretch or omit the truth when submitting their paperwork.

In many instances, people who commit soft insurance fraud don’t realise it’s fraudulent, and illegal. They may believe that “everyone stretches the truth” when they make claims, or they rationalise what they’re doing because they haven’t made a claim in a while, or have been paying insurance premiums for years.

There are more examples of soft and hard fraud on our website.

Do you know people making dishonest insurance claims?

Do the right thing! Do your friends and family a favour and tell them not to. Let them know that the actions they’re taking is considered soft fraud and a criminal offence. Importantly, if they get caught, a conviction can prevent their ability to get finance in the future.

You can also report insurance fraud by visiting our website. You can make reports anonymous if you wish.